.png)

Introduction

We were asked to write about choosing between a T14 school at sticker (full tuition) versus a T20 to T30 school with merit aid. The below constitutes our best stab at that, but please keep in mind that, as always, these are arbitrary cutoff points based on one flawed rankings system and not designed for you as an individual. Point being that a school ranked 18 may be much more valuable to you for any number of reasons that a school ranked 13, etc. If you want to read or watch more on the rankings, please read two of our blog posts here and here, or our YouTube video on rankings here. You can also check out MyRank, a tool we developed to make your own customized law school rankings prioritizing only the data you actually care about.

So, let’s dive into the question.

Cost of Attendance

The first thing we need to consider is what exactly “sticker” at a school costs. Sticker price won’t just be your tuition over three years—there are a good deal of other costs that applicants often don’t fully consider. Some are obvious, like the cost of living—your rent, utilities, food, transportation, etc. Schools will generally publish their estimated Cost of Living (COL) for the geographic area in which they are. Don’t count on working while in school to cover your lifestyle either. In fact, schools heavily frown on working your first year—ABA rules actually limit how many hours you could work even if you wanted to. Barring savings or external funding, you very well may be taking out significant loans for COL too.

There are also the less obvious costs. Health insurance, if you’ll need it. That can easily be a couple thousand dollars a year. Buying a new computer—schools usually give you a budget for a loan to do so, but that’s more debt. Tuition inflation is a big one. Every year schools increase tuition, usually between three and four percent. That might not sound like much, but when tuition is already sixty thousand dollars a year, that can be an extra five thousand dollars in debt by the time you graduate. You’ll need to pay loan origination fees every year—the exact amount will depend on how much you take out, but at sticker it’s easily over a thousand dollars every year. All the while the interest on your loans will be accumulating while you’re in school, and when the rates are between five and seven and a half percent, that adds up quickly.

Paying Back Debt and Job Opportunities at Top Schools

So let’s talk about paying back sticker debt. If you’re borrowing close to 100% of your Cost of Attendance (CoA) at a T14 law school, you will graduate with about $339,000 in loans. On a ten year repayment plan you would need to pay $3,936 dollars per month. Now of course you’re thinking, well okay, but I’m a T14 graduate—I’ll be in biglaw making piles of money. Yes, you probably will be; the odds are heavily in your favor. Even at the lowest ranked T14, Georgetown, 58.8% of graduates end up in biglaw or biglaw equivalent jobs (defined as graduates employed at firms with 100+ attorneys or federal clerkships). That number rises steadily the higher up in the T14 you go (to a point). Take a look at the table below.

This also needs a bit more disclaiming. 25% of Stanford graduates aren’t working at large firms or in clerkships, but a huge portion of that is probably because they achieved career outcomes more desirable to them, such as public interest or government work. Overall, though, these numbers work as a rough proxy for a school’s likelihood of placing you in a job where you can service your sticker debt. At most T14s, you have about a 75-80% chance of that outcome. Those aren’t bad odds.

But let’s take a look at the money you’ll be earning as a large firm associate.

That’s a ton of money, but it comes with a large disclaimer. Here is an example.

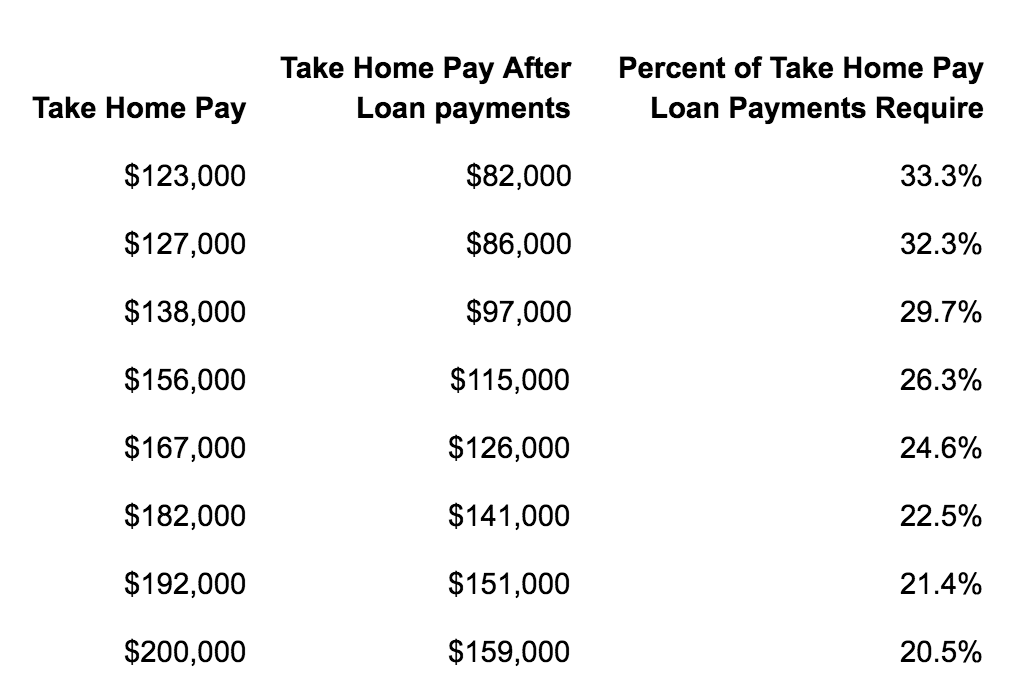

Suppose you’re a first year associate living and working in NYC. You’ll be earning $190,000 base salary—but after taxes and a (low) 5% 401k deduction, you’re taking home about $122,000 a year. That doesn’t account for any of your other costs, and you’ve already lost about a third of your salary. Let’s take a look at how much of your take home pay you’ll need to put towards loans on the standard ten year repayment plan of sticker debt. (Disclaimer, these are ESTIMATES ONLY; taxes etc. will vary.)

Many of us may have different perspectives when looking at these numbers. For some, they will see that even with massive sticker debt you can pay taxes and loans while still pocketing more than NYC’s median income every year. Fair point. Others may see the numbers and be shocked at how quickly that large salary gets eaten up. This is a personal decision that requires you to think long and hard about your personal financial goals and situation. But it is good to at least be aware of these numbers (and we are glad we were asked!).

It might be useful to look at a comparison: your earnings if you go into a non-biglaw job in New York City, starting off with a $60,000 annual salary. Here’s what your take home and loan repayment might look like over five years, assuming annual raises and enrollment in a PAYE repayment plan:

A PAYE plan will take you longer to pay off than the standard 10 year plan. But it will also give you much more financial freedom, especially if you don’t live somewhere as expensive and tax heavy as New York City. Further details on income driven repayment plans can be found here.

It’s also important to remember that the Biglaw life might not be sustainable for you. Large firms operate on an “up or out” model which starts to really push employees out after their third year. This can be market dependent. Right now there’s a strong demand for mid level associates, but that’s not always true. Demand for associates varies with economic conditions. Further, many biglaw associates leave the firms after a few years due to the grueling lifestyle and demands. This article goes into detail on a survey showing that almost half of all new associates leave their firms before the third year. Some will lateral into other firms making similar incomes, some will go into government or midlaw, some will leave law entirely. But the type of income you earn in biglaw—and thus the ability to service sticker debt—may not last. You know yourself and your dreams better than we do; do not let this dissuade those dreams. It is just another data point to consider. Macro data does not every dictate you as an individual.

Considering Other Options

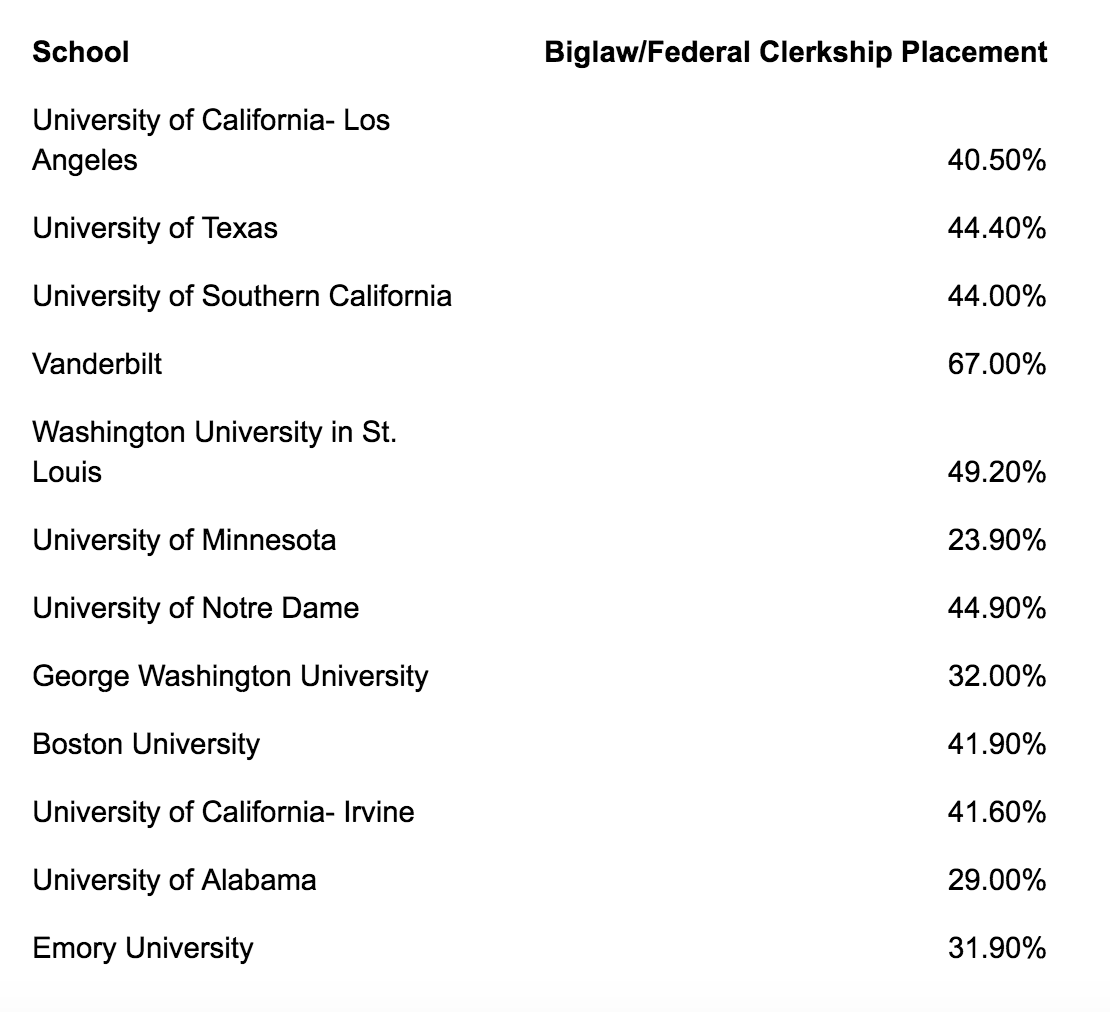

Many applicants who have been admitted to the T14 are weighing opportunities at lower ranked schools with scholarship assistance. Many of these schools are quite competitive for the elite outcomes available at T14 institutions. Below is a chart reflecting the placement success of the next twelve ranked schools.

As you can see, most students at these schools will not end up in the kinds of careers that can pay $300,000+ in loans. Many will, but the chances are lower here. However, if you’re a student considering one of these institutions with a scholarship or a T14 at full price, the equation becomes harder. Suppose you receive a full tuition scholarship to Boston University—a reasonably plausible outcome for someone who is also admitted to multiple T14 schools. At graduation, you would have around $85,000 in student loans—a quarter of what sticker price will cost you at a T14 school. Your monthly debt payments on a standard 10 year plan would be $990 dollars. Let’s take a look at what your biglaw take home pay might be after paying that kind of loan debt, with the same assumptions (NYC locale, 5% for 401k).

If you get a biglaw or equivalent job out of a T25, your take home pay after loans will be almost $30,000 more annually. That’s an extra $2,500 in your pocket every month—that adds up fast. Not everyone can get a full scholarship, but the point stands: less debt generally yields much more money in your pocket.

Of course, it’s also possible that you won’t get biglaw out of the T25. In that case, by taking the lower ranked school with a large scholarship, you’ve mitigated the downside—you will still have debt, but a substantially smaller amount (see PAYE table above). And that isn't to say you'll necessarily get a “bad job” if you strike out of biglaw. You can look at ABA employment data, found here. There's also easy to view versions of that data on www.lawschooltransparency.com. Both those are great sources of information on your possible range of outcomes at any given school.

Geographic Considerations

Another important consideration is where you want to be. T14s are generally (although look closely at each school in the T14; this isn’t always the case) considered to be able to place nationally—they may have a particular region in which they’re particularly strong, but what truly separates them from the rest is the portability of the degree. When choosing a T25 with a scholarship over a T14, the numbers suggest you’re sacrificing some regional mobility. 51.5% of T25 school graduates will end up working in the state they went to school. You can see the exact numbers on the chart below.

This isn’t to suggest it’s impossible to find an out-of-region job from a T25—far from it. But it’s harder than it is at a T14. For geographic placements, check ABA data and Law School Transparency for more details.

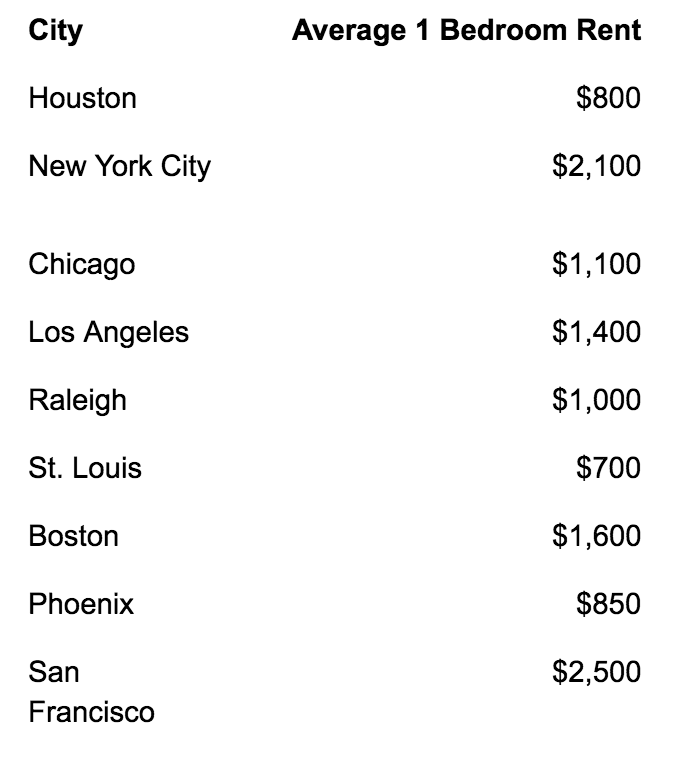

These are important factors to consider. If you want to work in a particular region, it would be prudent to check the placement power of the schools you are considering in that region. Geographic placement can also be important when considering your financial future and debt tolerance. Someone who is planning to live and work in Texas as opposed to NYC will have a larger take home check. Over the course of your first year working for a large firm, you’ll pocket another $10,000 while in Texas. Here’s a chart of a few sample cities and your approximate home pay in each.

Where you live can knock over ten thousand dollars off your annual salary, just in taxes. And then there’s cost of living. Take a look at this chart of the different cost to rent apartments in US cities:

Housing costs aren’t the only factor in cost of living, but it demonstrates the remarkable differences in how much you’ll need to live comfortably in different areas. Attending a school that places primarily in, for example, the Boston area leaves you less financial margin for error than one that places primarily in Arizona. Applicants may feel comfortable with taking out greater debt knowing they’ll have room in their budget thanks to low cost of living areas.

Considering Elite Outcomes

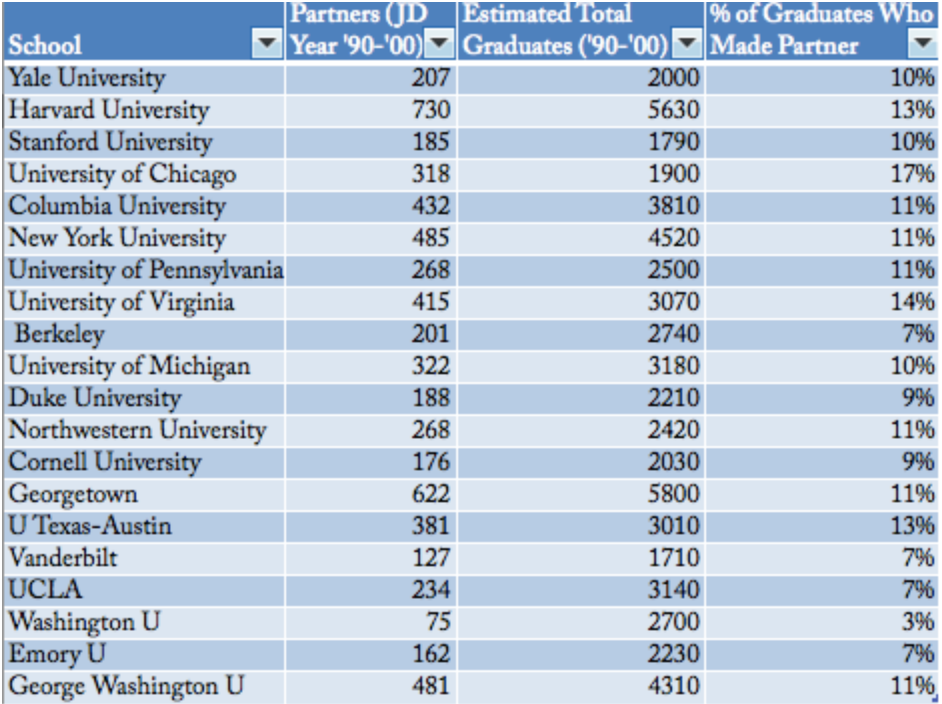

Some people may be interested in truly elite outcomes—the kind of opportunities that are rare outside of the top 14 schools. Applicants interested in these types of outcomes may be inclined to choose a higher ranked school, even with significant loan debt. Unfortunately, it’s tough to measure these kind of outcomes. Becoming a partner at a large firm is a great example of those kind of elite, hard to obtain outcomes. Take a look at this chart from a study by Michael Allen for an Above the Law article. It shows biglaw partner hiring from the top 20 law schools.

There are a few useful takeaways from this. First, within the top 14 schools, your chances of making partner generally don’t vary from school to school that much. It’s somewhere between a ten and fourteen percent chance (these numbers are likely lower today as fewer partners are being produced at firms). When you leave the top 14, there is a noticeable drop in the percent of graduates who make partner. It’s impossible to know every cause of this drop, but it’s reasonable to assume that the school you attended has at least some influence on your career within the firm—and a better school can, to a degree, improve your prospects within the firm.

SCOTUS clerkships are another way to measure these kinds of elite outcomes. The table below reflects the number of SCOTUS clerks each school has had since 2010. Only 8 schools have had 10+ SCOTUS clerks in that timeframe, and each of them is in the top 14 schools. In fact, the lowest ranked was the University of Michigan, ranked 9th in 2019.

These sorts of elite outcomes aren’t the only ones out there. But they’re easy to measure and serve to demonstrate how school rank and reputation can open up certain doors. If that’s something you’re interested in for yourself—and it’s okay if it’s not!—then make your decisions accordingly.

Conclusion

If you are choosing between a T14 at sticker or a T20/30, as we were asked to write about, congratulations, you have difficult choices. I like to think that Spivey Consulting is in the business of creating very difficult choices, and they are not confined to the above scenario but to all scenarios.

You can use this kind of cost-benefit analysis at any range of school. It’s not limited to comparing Top 14, Top 25, etc. schools with no scholarships and sticker debt. The mentality is what’s important here: thinking about your choices through the lens of how they’ll help you achieve your career goals, and how much of a financial sacrifice you’re willing and able to make for different likelihoods of achieving those outcomes.